Inheritance Tax (IHT)

Ins and outs

Like this page? Share it with your friends

Facebook

Twitter

LinkedIn

WhatsApp

Email

Print

Table of Contents

Introduction to Inheritance tax

Inheritance tax is a tax on the net chargeable estate of someone who dies. Landlords, particularly those with many properties, may well leave a high value estate when they die. As the rate of inheritance tax is 40%, the associated inheritance tax (IHT) bill may be significant.

There are however ways to potentially reduce the IHT payable on death, and even where a high IT bill is inevitable, it is possible to make provision in advance for the payment of that bill.

This article takes a look at some of the IHT considerations of relevant to landlords.

Nature of Inheritance Tax

Inheritance tax is often described as a voluntary tax. There is no tax to pay where the value of the estate is less than the available nil rate band, or where the estate is exempt because it is left to a spouse or civil partner, or to a charity or community amateur sports club.

There are various exemptions and relief which enable someone to make gifts free, or potentially free, of inheritance tax before they day.

However, property tends to be expensive and anyone with multiple properties is likely to have a chargeable estate in excess of the nil rate band. Even where property is left to a surviving spouse or civil partner on the first death and consequently no inheritance tax is payable, IHT will need to be considered in relation to the surviving spouse’s estate.

Inheritance Tax Nil Rate Band

A person can leave an estate free of inheritance tax up to the level of the nil rate band. The nil rate band has been set at £325,000 since 2009/10 and it is due to remain at this level for future tax years up to and including 2027/28.

Where a person has a main residence that they leave to a direct descendant, they may also be able to benefit from the RNRB. This is discussed at 30.2.4.

Transferable Inheritance Tax Nil Rate Band

Each spouse and civil partner has their own nil rate band. To enable a couple to leave everything to their spouse or civil partner without losing the benefit of their own nil rate band, the nil rate band is transferable between spouses and the portion of the unused nil rate band that is not used on the death of the first spouse or civil partner to die can be utilised on the by the estate of the surviving spouse or civil partner. As the amount transferred is the unused proportion of the nil rate band, rather than the absolute amount, there is an automatic adjustment for any change in the value of the nil rate band between the date of first death and the date of the second death.

The executors of the surviving spouse of civil partner must claim the unused nil rate band. This is done on form IHT217.

Transfer between spouses and civil partners are exempt from IT.

When undertaking Inheritance Tax planning, consideration should be given to how the nil rate band can best be used.

Case Study 1; Transferable Nil Rate Band

Arthur and Agnes have been married for many years. Agnes dies in 2016 and leaves her entire estate to Arthur. Arthur dies in 2023.

His estate is able to benefit from his own nil rate band, and also the unused portion (100%) of Agnes’ nil rate band.

The nil rate band available on Arthur’s death is therefore £650,000 – his own nil rate band of £325,000 and Agnes’ unused nil rate band of £325,000.

Residence Nil Rate Band

Estates can benefit from a second nil rate band – the residence nil rate band (RNRB)

– where a main residence is left to a direct descendant. While this will not shelter IHT on an investment property, it can potentially reduce a landlord’s IHT bill if the main residence qualifies for the relief.

The RNRB was introduced in 2017/18. It was set at £100,000 for 2017/18, £125,000 for 2018/19, £150,000 for 2019/20 and at £175,000 for 2020/21. It has remained at £175.000 since 2020/21 and is due to remain at this level for tax years up to and including 2027/28.

Unlike the nil rate band, the RNRB is only available in full if the value of estate is less than £2 million. For estates worth at least £2 million, the RNRB is reduced by £1 for every £2 by which the value of the estate exceed £2 million. This means that for 2020/21 to 2027/28 inclusive, the RNRB is not available where the value of the estate £2.35 million. Where an estate contains multiple properties, the value of the estate may very easily top £2.35 million, with the result that the benefit of the RNRB is lost.

As with the nil rate band, the unused proportion of the RNRB on the death of the first spouse or civil partner can be claimed by the estate of the surviving spouse or civil partner on their death. This remains the case even if the first spouse died before 6 April 2017 – the date on which the RNRB was introduced. The transferable RNRB must be claimed on IHT436.

The RNRB is also available where a person downsizes and sells or gives away their home on or after 8 July 2015 and leave other assets (such as the proceeds from the sale of their home) to a direct descendant.

The combined effect of the nil rate band and the RNRB is that a married couple or civil partners can between them leave up to £1 million free IHT, as long as a main residence worth at last £350,000 is left to direct descendants. A direct descendant is:

- A child, grandchild or other lineal descendant.

- The spouse or civil partner of a lineal descendant including their widow, widower or surviving civil partner).

A direct descendant includes a child who is or was at any time a step of child, a person’s adopted child, a child fostered by them at any time and a child in respect of whom the person was appointed as a guardian or special guardian when the child was under 18.

Siblings, nephews, nieces and other relatives not in the above list are not direct descendants.

Where the estate comprises the main home and other properties and some or all of the RNRB is available, to prevent the RNRB from being lost, where possible the main residence should be left to a direct descendant. For a couple, the RNRB can shelter IT of up to £140,000 (£350,000 @ 40%). From a tax perspective, a more favourable outcome is achieved by leaving the main residence to a direct descendant and, say, an investment property to niece or nephew, than vice versa.

If a particular property in the portfolio is to be left to a direct descendant, consideration could be made to making that property the main home to bring it within the scope of the RNRB.

Inheritance Tax Exemption for Gifts To Spouses And Civil Partners

Transfers to a spouse or civil partner who is domiciled or deemed to be domiciled in the UK are exempt from inheritance tax. The exemption applies to both lifetime and death transfers and is without limit, unless the transferor was UK domiciled and the transferee was non-UK domiciled at the time of the transfer.

This allows a married couple or civil partner to leave everything to their spouse without any inheritance tax arising on the death of the first spouse or civil partner, irrespective of the value of their estate.

However, this may not always be the best solution from a tax perspective and in certain circumstances in can be beneficial to leave assets up to the value of the available nil rate band other than to the surviving spouse or civil partner.

Potentially Exempt Transfers for Inheritance Tax

Lifetime gifts are potentially exempt from inheritance tax and are termed ‘potentially exempt transfers’ (PETs). The gift will only become chargeable to IHT if the transferor does not survive for seven years from the date of the gift. However, if the transferor survives at least three years from the date of the gift, the rate of tax that is applied to the gift is reduced. The percentage of the full tax charged and the effective rate of tax for gifts in the seven years prior to death is shown below.

Years between date of gift and death | Percentage of tax charged

| Rate of tax on the gift |

0 to 3 years | 100% | 40% |

3 to 4 years | 80% | 32% |

4 to 5 years | 60% | 24% |

5 to 6 years | 40% | 16% |

6 to 7 years | 40% | 8% |

7 or more years | 0% | 0% |

However , as the nil rate band is allocated to gifts in chronological order, the rate of tax sheltered by the nil rate band may be less than 40% where it is set against a PET that would otherwise have benefitted from taper relief.

While giving away assets prior to death can be beneficial from an IHT perspective, particularly if the donor survives seven years, IHT is not the only tax that needs to be considered when making a gift.

This is explored further in section 30.6.

Inheritance Tax: Gifts Out Of Income

A person can make regular gifts out of their income without any IT consequences, as long as the person can afford to make the payments after they have met their living ‘normal expenditure out of income’

costs and the gifts are paid from their regular income. Such gifts are referred to as

For a landlord with multiple rental properties and rental income in excess of that needed to meet their day-to-day living costs, this can be a useful exemption and can be used to prevent income from accumulating and forming part of the estate a death. However, the exemption only applies to regular payments and it is prudent to set up a direct debit or standing order to make the payments. For example, surplus income could be used to pay a child’s rent or a grandchild’s school fees.

This exemption can also be used where an IHT bill is inevitable to provide funds to pay that bill.

Inheritance Tax: Annual Exemption

An annual exemption of £3,000 applies for IHT purposes which allows a person to give away gifts worth £3,000 in total each tax year without them being added to their estate The annual exemption can be used to give gifts or £3,000 to one person or gifts totalling £3,000 to several people. Where the annual exemption is not used on year, it can be carried forward to the following year (meaning that a person can make up to £6,000 of tax-free gifts in that year).

If the unused exemption is not used in the following year, it is lost. The current year exemption must be used before any unused exemption from the previous tax year.

Inheritance Tax: Other Exempt Gifts

A person can give as many gifts of up to £250 per person in a tax year, as long as the recipient has not benefitted from another allowance (such as a gift on marriage).

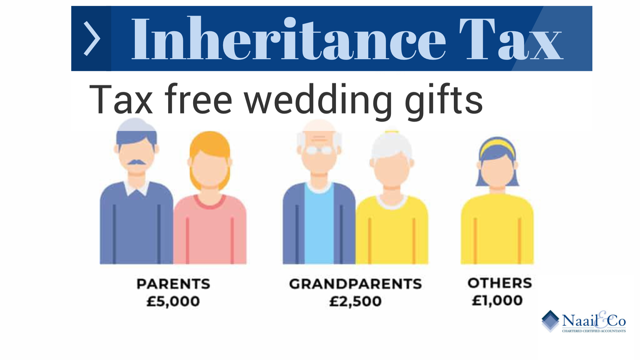

Tax-free gifts can also be made on the occasion of a marriage or a civil partnership.

The exemption applies to gifts of up to £5,000 where the recipient is a child, gifts of up to £2,500 where the recipient is a grandchild or great-grandchild and £1,000 where the recipient is another person. A wedding gift can be combined with another allowance (such as the annual exemption), with the exception of the small gifts allowance.

Gifts made out of regular income, for example birthday and Christmas gifts can be made without limit. The exemptions limit tax-free gifts that can be made from capital.

Inheritance Tax: Business Property Relief

Business property relief (BR) reduces the value of a qualifying business or assets when working out how much IT has to be paid on the estate. There are two rates of BPR – 100% and 50%. The relief applies where qualifying property is passed on while the transferor is alive or as part of the Will. Relief can be claimed on property and building, unlisted shares and machinery.

BPR at 100% is available on:

- A business or interest in a business.

- Shares in an unlisted company.

BPT at 100% is available on:

- Shares controlling more than 50% of the voting rights in a listed company.

- Land, buildings or machinery owned by the deceased and used in a business in which they were a

partner or which they controlled.

- Land, buildings or machinery used in the business and held in a trust that it has the right to benefit from.

To qualify for the deceased must have owned the business or the asset for at least two years before they died.

BPR is not available where the company mainly deals in securities, stocks or share, land or buildings or the holding of investments. The final restriction poses something of a problem for landlords looking to access BPR.

BPR is not available on an asset that also qualifies for agricultural property relief. Relief is also denied if the asset was not used mainly for the business for at least two years prior to the deceased’s death or if the asset isn’t needed for the future of the business.

Inheritance Tax: Agricultural Relief

Agricultural property relief (APR) is available on a qualifying transfer of agricultural property, such as farmland and farm buildings (including farm cottages and farmhouses). Properties may be owned or let but must be part of a working farm. The property must have been owned for at least two years prior to the deceased’s death where occupied by the owner, a company controlled by them or their spouse or civil partner and for at least seven years before the deceased’s death if occupied by someone else. Properties must be occupied by someone employed in farming, a retired farm employee or the spouse or civil farmer of a deceased farm employee to qualify for the relief. The properties must also be of a size and nature to the farming activity taking place.

APR at 100% is available where:

- The person who owned the land farmed it themselves.

- The land was used by someone else on a short-term grazing licence.

- The land was let on a tenancy that commenced on or after 1 September 1995.

Relief is available at 50% in all other cases.

Transfers of agricultural land and buildings and farm equipment that do not qualify for

APR may qualify for BPR.

Inheritance Tax: Making Use Of Exemptions And Relief

Landlords looking to mitigate the IT payable on their death should make best possible use of the nil rate bands and the available reliefs and exemptions. Strategies for doing this are discussed later in this chapter.

It is never too early to take inheritance tax planning advice, and when purchasing properties or making business decisions, the IHT implications should be taken into consideration. There is no one size fits all and the best strategy for you will depend on your personal circumstances and what you want to achieve. IHT planning should be undertaken as part of wider succession planning goals.

TIPS & FAQs

1. When do I need to start planning?

As early as possible as your circumstances and exposure to IHT will change over time. Early on, an insurance policy might be all that is necessary but more complex planning will be appropriate as wealth increases.

2. Can I afford to make lifetime gifts?

A good tool is a professional cash flow forecast which is updated regularly. You can plan in major life events (such as marriage, holidays, care fees) and see what your overall position is.

3. Is planning only for the wealthy?

No – many people have been pushed into the IHT net due to increases in property values.

4. What is the current nil rate band?

The current nil rate band is £325,000 per person. This can be used against both lifetime transfers and transfers on death. It effectively ‘refreshes’ every seven years. Any unused nil rate band as at the date of death can be transferred to a surviving spouse for use on their death.

5. What is the residence nil rate band?

This is a further nil rate band of up to £175,000 which is available if the residential property is passed to lineal descendants. It is only available against the death estate, but any unused relief can be passed to a surviving spouse. The relief is tapered for estates in excess of £2m.

6. Can I make lifetime gifts free of IHT?

Yes, the nil rate band can be set against lifetime gifts as well as on death. There is also an annual exemption of £3,000 – this can be rolled forward up to one tax year. In addition to this, small gifts of up to £250 and gifts out of excess income can be made to anyone free of IHT. You can also make gifts of between £1,000 and £5,000 (depending on the relationship to the giftee) in consideration of marriage or civil partnership.

7. Is it tax efficient to make gifts to charity?

Yes – gifts to charity are tax exempt and if you leave at least 10% of your net estate to charity, the rate of IHT is reduced to 36%.

8. I have a business. Will that be exempt?

Business property relief of up to 100% is available for businesses and shares in certain companies, as well as some assets that are held personally, but used by the business/company. However, it is easy to taint this if investment assets or excess cash are held within a trading business.

9. Can I leave my estate to my spouse tax free?

Yes, if the estate is left to a surviving spouse, this is tax free. The surviving spouse will also inherit any unused nil rate band and residence nil rate band. Bear in mind that this will increase the spouse’s estate for IHT so may only be delaying the problem.

10. Can I pass on my pension tax free?

Yes, you can pass on a pension pot tax IHT free. It is therefore better to draw down on cash assets (bank accounts, ISAs, etc) in priority to the pension as those assets will be subject to IHT on death. In the Spring Budget, the Chancellor abolished the lifetime pensions allowance and the annual cap on tax-free pensions contributions was increased to £10,000 a year. These changes have made pensions potentially even more valuable for IHT planning as you can pay more into your pension, and still have access to your funds should something unexpected happen.

Our service to you

If you are a self employed, business owner/director of company looking to get your accountancy and taxation matters sorted, look no further. We are pro-active and easily accessible accountants and tax advisors, who will not only ensure that all your filing obligations are up to date with Companies House and HMRC, but also you do not pay a penny more in taxes than you have to. We work on a fixed fee basis and provide same day response to all your phone and email enquiries. We will also allocate a designated accounts manager who would have better understanding of your and business financial and taxation affairs. Book a free consultation call with one of our inheritance tax accountants using the link below.

Related pages:

Get further information from the following pages;

Related Blogs:

Get further information from the following blogs;

How to cut inheritance tax bill

Inheritance tax planning for main residence

Inheritance tax: Gifts for maintenance of family

Subscribe to our newsletter

BUSINESS HOURS

Monday – Friday

- 9:00 am – 5:30 pm

Pages:

Menu